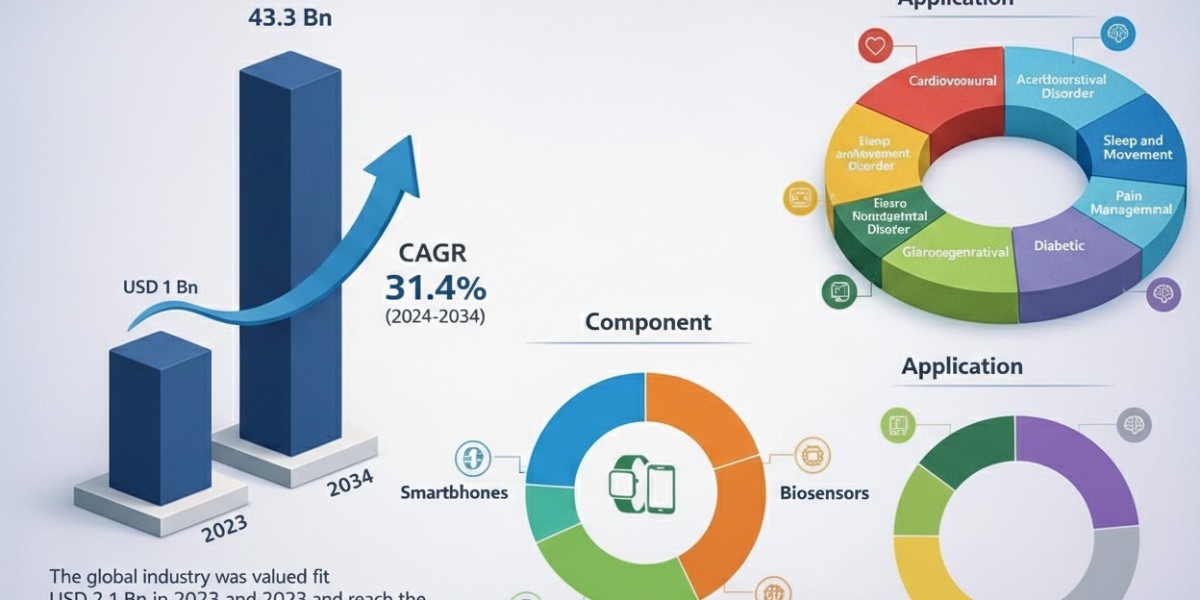

The global digital biomarkers market was valued at USD 2.1 billion in 2023 and is projected to surge to USD 43.3 billion by the end of 2034. This remarkable expansion reflects the rapid adoption of wearable devices, mobile health applications, and AI-driven analytics in clinical research and personalized medicine. The industry is expected to grow at a robust CAGR of 31.4% from 2024 to 2034, driven by rising demand for remote patient monitoring, early disease detection, and data-driven healthcare solutions.

The digital biomarkers market is growing on the basis of an exorbitant increase in incidence of chronic diseases. Digital biomarkers proffer noteworthy interpretations of digital measurements of a patient along with correlated medical conditions. They capture and analyze array of environmental, behavioral, and physiological data through wearables, sensors, and digital platforms.

Transform Your Strategy: Explore In-Depth Data – Sample Available! https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=79554

The key players in digital biomarkers market are working toward increasing psychophamacology clinical trial success rates with biomarkers and digital measures. They are also exploring the probability of using digital biomarkers for Parkinson’s disease. Application of AI to digital biomarkers in order to improve diagnosis and reduce readmissions is on the anvil.

Market Segmentation

By Service Type

- Data Collection Services: Capturing raw data from sensors and apps.

- Data Analysis & Integration: Using AI/ML to convert raw data into clinical insights.

- Consulting & Strategic Services: Helping pharma companies integrate biomarkers into drug development.

By Sourcing Type

- In-house: Large pharmaceutical firms developing proprietary digital endpoints.

- Outsourced: Increasing reliance on specialized digital health startups (e.g., Koneksa, Empatica) for validation and technology.

By Application

- Cardiovascular Diseases: The largest segment in 2024, focusing on heart rhythm and blood pressure monitoring.

- Neurological Disorders: Tracking tremors (Parkinson’s) and cognitive decline (Alzheimer’s).

- Metabolic Diseases: Continuous glucose monitoring (CGM) and obesity management.

- Sleep and Movement Disorders: Analyzing sleep cycles and physical mobility.

- Psychiatric Disorders: Monitoring mood and behavior via smartphone usage patterns.

By Industry Vertical (End-User)

- Pharmaceutical & Biotechnology Companies: Use in clinical trials to reduce costs and increase success rates.

- Healthcare Providers: Integration into hospitals for remote patient monitoring.

- Payers: Insurance companies using data to incentivize healthy behaviors.

Regional Analysis

- North America: The dominant region, holding over 58% market share in 2024. Growth is fueled by high healthcare spending, a robust regulatory environment (FDA Pre-Cert program), and the presence of tech giants like Apple and Google.

- Asia-Pacific: Predicted to be the fastest-growing region (CAGR ~23.5%). Driving factors include massive smartphone penetration in China and India, alongside government-led digital health initiatives (e.g., India’s Ayushman Bharat Digital Mission).

- Europe: Significant growth driven by the EU4Health program and strict data privacy standards (GDPR) which are fostering "trust-based" digital health adoption.

Market Drivers and Challenges

Drivers

- Rising Prevalence of Chronic Diseases: 60% of US adults live with at least one chronic condition, requiring continuous monitoring.

- AI and Machine Learning: Advanced algorithms can now identify "sub-clinical" changes that are invisible to the human eye.

- Regulatory Support: The FDA’s "Fit-for-Purpose" initiative and software-as-a-medical-device (SaMD) guidelines are streamlining approvals.

- Cost Efficiency: Reducing the need for in-person clinic visits and speeding up clinical trial timelines.

Challenges

- Data Privacy & Security: Handling sensitive health data remains a significant risk for cyberattacks.

- Lack of Standardization: Difficulty in comparing data across different devices (e.g., an Apple Watch vs. a Fitbit).

- Clinical Validity: Many digital markers still lack the rigorous clinical "proof" required to replace traditional gold-standard tests.

Market Trends & Future Outlook

- Vocal Biomarkers: Using "voice as a vital sign" to detect depression, anxiety, and respiratory issues.

- Decentralized Clinical Trials (DCTs): A permanent shift toward monitoring trial participants at home rather than at clinical sites.

- Generative AI Integration: Future systems will likely use LLMs to provide patients with real-time, conversational feedback based on their biomarker data.

Competitive Landscape

The market is characterized by a mix of established tech firms and specialized biotech players:

- Tech Giants: Apple, Google (Fitbit), Samsung.

- Specialized Players: AliveCor (ECG), Empatica (Physiological sensors), Koneksa Health, BioSensics, Huma.

- Pharma Collaborators: Roche, Biogen, and AstraZeneca are increasingly embedding digital biomarkers into their drug portfolios.

Recent Developments (2024-2025)

- In March 2023, Koneksa announced that it had launched a clinical study that compared outcome between at-home mobile spirometry using digital biomarkers and in-clinic spirometry in the patients suffering from modern asthma on long-acting beta-agonist (LABA) treatment.

- In January 2023, Aculys Pharma, Inc. entered into research collaboration with Four H, Inc. to enable usage of wearable devices for helping individuals with excessive daytime sleepiness and narcolepsy linked with obstructive sleep apnea syndrome (OSAS).

Elevate Your Business Strategy! Purchase the Report for Market-Driven Insights: https://www.transparencymarketresearch.com/checkout.php?rep_id=79554<ype=S

Key Market Study Points

- The Wearable Segment remains the primary revenue contributor, but Mobile Apps are the fastest-growing sub-segment.

- The transition from Reactive to Proactive care is the fundamental value proposition.

- Interoperability between digital biomarkers and Electronic Health Records (EHR) is the "final frontier" for mass clinical adoption.

About Transparency Market Research

Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information.

Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports.

Contact:

Transparency Market Research Inc.

CORPORATE HEADQUARTER DOWNTOWN,

1000 N. West Street,

Suite 1200, Wilmington, Delaware 19801 USA

Tel: +1-518-618-1030

USA – Canada Toll Free: 866-552-3453

Website: https://www.transparencymarketresearch.com

Email: sales@transparencymarketresearch.com